Trust / Financial Services / 1958-present

American Express Branding Case: Membership and Payment Trust

American Express is the payment-brand case for making membership, merchant acceptance, rewards, service, cardholder trust, and dispute confidence carry a premium finance promise.

Short Answer

American Express Branding Case: Membership and Payment Trust is a trust case about American Express in 1958-present. American Express turns a payment card into a status and service system when the customer can use acceptance, benefits, protection, rewards, and support as proof. Premium payment brands need evidence at both sides of the transaction: cardmember confidence and merchant acceptance. Status language breaks if the card is hard to use or hard to resolve.

Reader Task

What this entry should help you finish

Use this entry to finish four jobs: answer what happened to American Express, see why it belongs in the trust lane, inspect the decision consequence, and leave with the operator lesson. The point is not to remember the brand. The point is to know what decision, proof surface, or failure mode a team should check next. Then compare it with Huawei, NIVEA, Honda before turning the case into a rule.

What American Express teaches

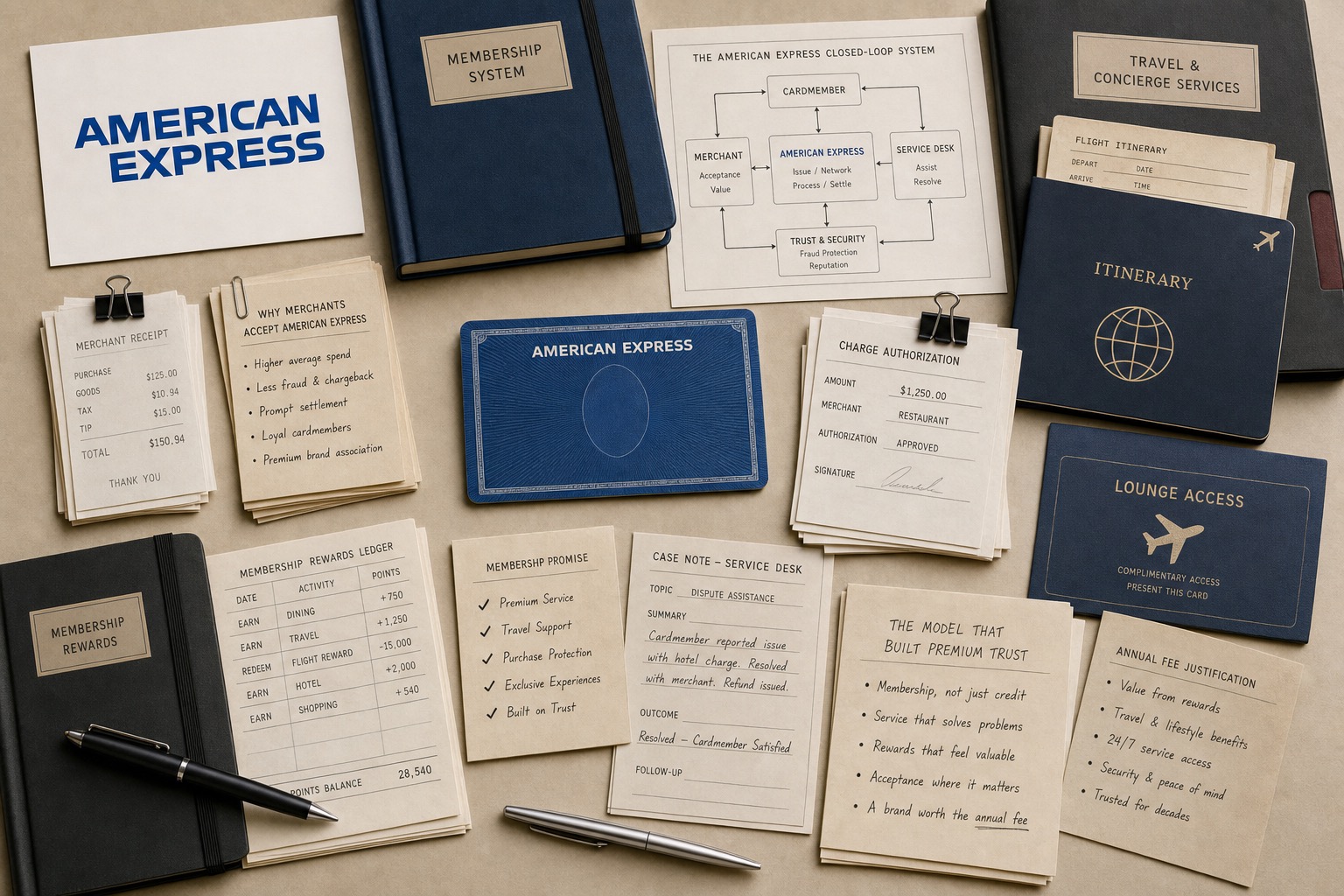

- American Express is more than a card design case. It is a membership and service case because the promise is judged when money, access, rewards, and recovery are at stake.

- The closed-loop model gives the company more control over cardmember and merchant data, but that control has to become a better customer experience.

- Rewards and travel benefits can increase loyalty only when redemption, fees, acceptance, and service stay understandable.

- Merchant acceptance is part of the brand because a premium card loses meaning at the moment it is refused.

- The weak copycat uses elite language before it has service, benefits, and dispute handling that deserve the fee.

Why This Brand Belongs In The Archive

American Express belongs in The Brand Archive because the page studies a specific brand decision, not a company profile. The decision sits in trust and gives operators a way to see how trust changes commercial value.

The useful archive question is what changed in recognition, trust, demand, pricing power, category position, or public memory after the market saw the move.

The Brand Asset At Stake

The asset at stake is access, transaction confidence, service recovery, and visible risk control. That asset matters because it affects how people find, understand, choose, trust, or repeat the brand when the company is not in the room to explain itself.

For American Express, the asset is not abstract equity. It has to show up in the buying surface, product surface, service route, source record, or repeated customer behavior.

What Changed

American Express turns a payment card into a status and service system when the customer can use acceptance, benefits, protection, rewards, and support as proof.

The change forced the market to decide whether the old shortcut still worked, whether the new proof was strong enough, and whether the brand had made the category easier or harder to understand.

What The Market Learned

The market learned to judge American Express through the gap between the visible move and the proof behind it. calling the brand trusted while avoiding the proof of access, error handling, fees, service, and recovery is the weak reading this page is meant to prevent.

A useful brand decision makes buying, remembering, trusting, or repeating easier. A weak decision makes the audience do more work before it believes the claim.

Commercial Consequence

The commercial consequence sits in trust: access, transaction confidence, service recovery, and visible risk control. When that proof becomes easier to see, customers have more reason to choose, trust, repeat, or pay attention. When it becomes harder to see, the brand has to spend more money explaining what the market used to understand faster.

American Express matters because the decision changed more than presentation. It changed buyer confidence, memory, category position, or repeat behavior in financial services. That is why the case belongs in a brand decision library instead of a general company profile.

What Another Brand Should Learn

Another brand should use this case before spending money on a similar move. Name the customer behavior, the proof surface, the protected cue, and the consequence that would make the decision worth the cost.

If the same proof does not exist in the business, copying American Express would copy the surface while missing the reason the decision mattered.

The Decision Context

American Express has to sell a finance product that is both practical and symbolic. The card must work at checkout, but the brand also asks customers to treat membership, service, rewards, and access as worth more than a cheaper payment route.

That makes the case harder than a status story. The premium signal has to survive ordinary payment friction: acceptance, fees, disputes, benefits, account management, travel changes, and merchant relationships.

Membership Is A Contract, Not A Mood

Membership language gives American Express a distinctive frame. It implies belonging, recognition, service, and a higher standard than a commodity payment product.

That language works only if the cardmember can point to specific benefits: rewards, protection, travel support, offers, service access, and a clearer recovery path when something goes wrong.

Merchant Acceptance Carries The Promise

A payment brand fails in public when the customer reaches the counter and cannot use it. Merchant acceptance is therefore part of brand meaning, not an operations footnote.

American Express has to balance merchant economics with cardmember value. The brand stays strong when acceptance, merchant services, and cardmember benefits reinforce each other instead of creating friction.

Rewards Need Clear Value

Membership Rewards can create loyalty because the points make repeated spending visible. The risk is complexity. If earning, transfer, redemption, fees, and restrictions become too hard to read, the benefit becomes weaker than the headline.

The best reward system teaches the customer what to do next. A premium brand should not require the customer to decode value alone.

Service Is The Premium Proof

Service is where American Express can justify a higher frame. Fraud support, disputes, travel help, account servicing, and card replacement are the events where a finance brand becomes personal.

Those events matter because the customer is often under pressure when they need help. A premium promise is credible only when the recovery path is clearer than the alternative.

Where The Strategy Breaks

The strategy breaks when status outruns usability. A prestigious card that is refused, hard to redeem, or slow to support becomes a contradiction.

The second break is benefit inflation. Adding more perks can make the product harder to understand if the customer cannot tell which benefit solves which problem.

The Bad Copycat

A bad copycat would borrow black-card language, lounge imagery, metal-card cues, and VIP vocabulary before building a real payment, merchant, reward, and service system.

That move creates a costume of premium. The customer finds out quickly whether the brand can actually protect the transaction.

The Archive Reading

American Express is filed here because it records how membership can turn a payment instrument into a broader trust contract.

The decision test is whether every premium signal points to usable proof: acceptance, service, rewards, protection, account clarity, and recovery power.

The Decision Pressure

American Express has a sharper proof burden than an ordinary payment product because the buyer is often paying for a relationship, more than a transaction rail. The cardmember wants acceptance, benefits, protection, rewards, and service to add up to a reason for the fee.

That pressure appears when the customer is away from home, facing a disputed charge, redeeming points, renewing a card, or asking a merchant to accept the network. The brand either lowers anxiety at that moment or the premium story becomes thin.

The page should teach that membership is a repeated service test. A finance brand can look prestigious in the wallet and still fail if the transaction, benefit, or recovery path is hard to use.

Compare Next

Related Cases

Do not read American Express alone. Compare it against nearby cases: Huawei, NIVEA, Honda.

Sources

{kind=link}

.svg){kind=link}

People Also Ask

What happened to American Express?

American Express Branding Case: Membership and Payment Trust is a trust case about American Express in 1958-present. American Express turns a payment card into a status and service system when the customer can use acceptance, benefits, protection, rewards, and support as proof. Premium payment brands need evidence at both sides of the transaction: cardmember confidence and merchant acceptance. Status language breaks if the card is hard to use or hard to resolve.

Why is American Express a trust case?

American Express is filed as a trust case because the visible consequence sits in that decision pattern. American Express turns a payment card into a status and service system when the customer can use acceptance, benefits, protection, rewards, and support as proof.

What can brands learn from American Express?

Premium payment brands need evidence at both sides of the transaction: cardmember confidence and merchant acceptance. Status language breaks if the card is hard to use or hard to resolve.

Is American Express still operating?

The Brand Archive marks American Express as Active / continuing. That means the brand, company, platform, product system, or parent organization is still operating, continuing, or being actively resolved.

What should American Express be compared with?

Compare American Express with Huawei, NIVEA, Honda to see the same decision pattern from nearby cases.