Rebrand / Financial Services / 2016-2019

Mastercard and the Symbol That Could Stand Without the Name

Mastercard's move to a wordless symbol worked because the interlocking circles had already accumulated enough global payment memory to carry acceptance, trust, and network recognition on their own.

Short Answer

Mastercard and the Symbol That Could Stand Without the Name is a rebrand case about Mastercard in 2016-2019. A payment-network identity reached the point where the symbol could carry the name's job: acceptance, speed, trust, and global recognition at the moment of transaction. Wordless identity only works after memory has been earned. Removing the name is a governance decision about recognition equity, not a minimalist design trick.

Key Takeaways

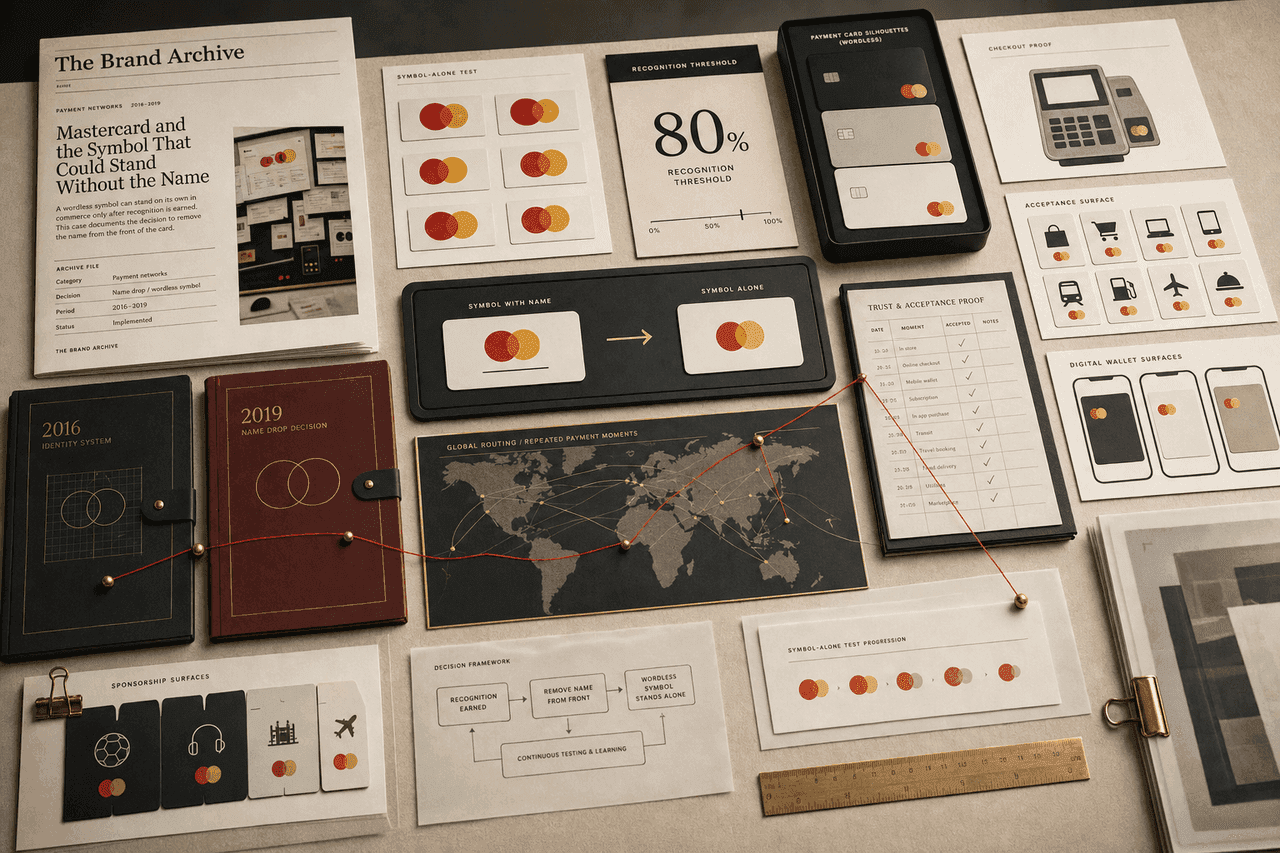

- Mastercard modernized its identity system in 2016 while keeping the name visible, then moved further in 2019 by dropping the word Mastercard from the brand mark in many contexts.

- Mastercard's 2019 announcement said more than 80 percent of people spontaneously recognized the Mastercard Symbol without the word.

- The 2019 change applied to high-repetition surfaces: cards, acceptance marks at physical and digital retail locations, and major sponsorship properties.

- In payments, the symbol does more than identify a company. It signals acceptance, trust, routing reliability, and a familiar checkout path.

- The case is positive because simplification followed recognition. The company was not asking customers to recognize something unearned.

The Decision Context

Financial-services marks have a different job from ordinary consumer logos. They appear at the moment of trust: card in hand, terminal in front of the customer, merchant sign on the door, wallet option on a screen, cross-border transaction moving through infrastructure the user cannot see.

That is why Mastercard's wordless move matters. The company was not merely making a logo cleaner. It was deciding that the symbol itself had enough accumulated meaning to carry the acceptance signal without the written name sitting beside it.

The 2016 System

Mastercard's 2016 identity work simplified and modernized the brand system while keeping the name visible. The interlocking circles became cleaner, flatter, and more flexible across digital and physical contexts, but the wordmark still helped the public connect symbol and name.

That intermediate step matters. A brand does not have to remove language all at once. It can train recognition through a disciplined system first, then test whether the nonverbal asset can carry more of the burden.

The Recognition Threshold

The 2019 decision had a hard proof point. Mastercard said more than 80 percent of people spontaneously recognized the Mastercard Symbol without the word. That number changes the reading of the case. The company was not relying on taste, executive confidence, or a design trend. It had public recognition evidence before removing the name from many uses.

The threshold matters because wordless identity is a transfer of burden. The word had been doing part of the identification job. Once the word disappears, the symbol has to carry recognition, category, acceptance, and trust by itself. If the mark cannot do that under real conditions, the cleaner system is weaker.

The 2019 Name Drop

In January 2019, Mastercard announced that the company would drop the name from the brand mark in many contexts. The announcement named the surfaces: cards using the red and yellow mark, acceptance marks at retail locations in the physical and digital worlds, and major sponsorship properties.

The important point is sequence. The circles were already attached to paying, being accepted, moving money, and seeing the same signal across countries and channels. The word could disappear because memory had already done the work.

Where The Symbol Had To Work

Payment-network brands are unusually repetitive. A customer sees the mark on cards, terminals, checkout screens, merchant doors, airport signage, stadium sponsorship, banking pages, and wallet interfaces. Every accepted transaction reinforces the symbol as a permission signal.

That repetition creates network memory. The mark becomes shorthand for a transaction path that works. If the symbol is visible and the payment goes through, the brand earns another proof point. Over time, those proof points become recognition equity.

This is why the same visual move would be riskier for a weaker brand. Mastercard did not remove the name from a low-frequency surface. It removed the name from a symbol that customers and merchants had already seen in the exact moment where the brand had to reduce risk.

The Risk

Dropping a name can look elegant in a boardroom and confusing in the market. The risk is especially high when the symbol is still dependent on the word for meaning. Without enough memory, wordless identity becomes a guessing game.

Mastercard avoided that problem because the circles were already the asset. The name was important, but the checkout moment often gave the symbol its practical meaning faster than language could. A user did not need to read Mastercard to understand that the payment network was present.

What This Case Does Not Prove

The Mastercard case does not prove that every brand should chase a wordless logo. It proves the opposite: a wordless mark needs earned memory, repeated use, disciplined rules, and a decision context where the symbol can do the job faster than language.

The shallow copy of this move is to remove the word because the mark looks cleaner. The useful copy is procedural. Keep the name while recognition is being trained. Measure whether the symbol works alone. Remove words only where the customer already understands the signal.

Operator Test

Before removing a name, ask four questions. First, what percentage of people recognize the symbol without the word? Second, which exact surfaces will carry the wordless mark? Third, what customer risk appears at those surfaces? Fourth, what bridge keeps the old cue available if recognition falls?

If the team cannot answer those questions with evidence, the cleaner identity is not ready. If it can, the change becomes a governance decision: use the name where language still helps, and let the symbol work where memory has already been earned.

The Decision Lesson

Mastercard belongs in the archive as a positive identity-simplification case. It shows that minimalism is safest when it follows evidence. The symbol had earned recognition through use, infrastructure, consistency, and repetition.

For leaders, the lesson is to ask what part of the identity actually carries recognition in the customer's moment of decision. If the symbol has not earned that role, removing the name is vanity. If it has, simplification can make the brand faster, more universal, and easier to deploy across new contexts.

Where The Strategy Can Break

Mastercard should not be read as a clean success label. The useful question is where the rebrand promise can fail in the real category: customers are being asked to place money, identity, credit, or protection inside the system.

The weak reading is calling the brand trusted while avoiding the proof of access, error handling, fees, service, and recovery. That kind of page sounds polished but gives the reader no way to judge the decision.

The concrete failure mode is this: the public remembers the friction point first: a blocked account, a confusing fee, a failed claim, a poor branch handoff, or a weak digital recovery path. If the case cannot explain that risk, the brand story is not finished.

The Bad Example

A bad Mastercard copycat would start with the visible surface: the mark, the color, the store, the app, the route, the campaign, or the public phrase. Then it would assume the surface created the result.

That is usually backwards. The surface worked only if the category proof underneath it was already strong enough: access, transaction confidence, service recovery, and visible risk control.

The page has to protect readers from that shortcut. The mistake is not ambition. The mistake is copying the artifact while leaving the constraint untouched.

What To Copy

Copy the discipline, not the costume. For Mastercard, the discipline sits in the link between financial services pressure, customer behavior, and the proof a buyer or user can inspect.

A useful reader should be able to point to one behavior that changed, one risk that dropped, and one cue that helped the change stick.

If those three pieces are missing, the page should not pretend the case is a repeatable playbook. It is only a brand example with missing machinery.

The Proof Trail

Start with the year or period: 2016-2019. Then ask what was visible to the market at that time, what changed after the decision, and what evidence still exists now.

The source list gives the inspection trail. Use it to separate what Mastercard says about itself from what the case page argues about the brand decision.

The proof should answer five checks: money or protection risk, access proof, service recovery, fee or claim clarity, regulatory and trust burden. If the page cannot answer them, the case needs more source work before anyone treats it as a decision record.

The Decision Limit

The case should not be used as a slogan for doing the same thing. It should be used as a boundary test. The question is whether the same market pressure, customer behavior, proof surface, and timing exist before the decision gets copied.

Mastercard gives the archive a concrete inspection point: access, transaction confidence, service recovery, and visible risk control. If a team cannot point to that proof in its own business, the comparison is weak, even when the visible asset looks similar.

The better lesson is operational. Decide what must be true before the cue, campaign, name, product, route, or experience can carry the promise. Then decide which signal would stop the move if customers reject it, ignore it, or use it in the wrong way.

A serious reader should leave with a constraint, not a mood. For Mastercard, the constraint sits in financial services: who is choosing, what risk they are managing, which proof they can inspect, and what would make the promise collapse under normal use.

The final check is the comparison set. Put Mastercard beside two adjacent cases and ask what changed in each file: the cue, the behavior, the channel, the proof, the public language, or the operating burden. The answer keeps the case from becoming trivia.

This is where the archive page earns its keep. It turns a brand story into a decision memo: what changed, who had to believe it, what proof reduced the risk, what failure would expose the gap, and which nearby cases warn against copying the surface too quickly.

Case Depth

Why This Case Matters

Mastercard matters because it shows when simplification is evidence-based. The name could step back only after the circles had already done the acceptance job in the customer's payment moment.

The case is high-value for visual identity, brand guidelines, salience, and rebrand risk because it separates earned recognition from decorative minimalism.

Operator Misread

What Operators Usually Misunderstand

- The shallow reading is that Mastercard proved wordless logos are modern. The better reading is that the company removed words only after decades of payment-context repetition had trained the symbol.

- Operators often ask whether a simplified mark looks clean. Mastercard shows the harder question: will the cue still reduce risk at the exact moment of use?

Source-Backed Timeline

The Decision Timeline

- 2016 Mastercard modernized the identity system while keeping the name visible beside the interlocking circles.

- January 2019 Mastercard announced that the name would be dropped from the brand mark in many contexts because the symbol had strong recognition.

- Checkout use Cards, merchant doors, payment terminals, wallet interfaces, and sponsorship surfaces kept repeating the same acceptance cue.

- Current recognition job The symbol has to carry payment acceptance, speed, trust, and global network memory on small digital and physical surfaces.

Comparable Cases

Sources

- Mastercard Newsroom, Mastercard evolves its brand mark by dropping its name, January 7, 2019

- Mastercard Brand Center, Brand History

- Mastercard Brand Center, Mastercard Brand Mark guidelines

- Pentagram, Mastercard identity case study

- WIRED, Why You Recognize Mastercard's New Logo, July 2016

- Wikimedia Commons, Mastercard 2019 logo file

{kind=link}

People Also Ask

What happened to Mastercard?

Mastercard and the Symbol That Could Stand Without the Name is a rebrand case about Mastercard in 2016-2019. A payment-network identity reached the point where the symbol could carry the name's job: acceptance, speed, trust, and global recognition at the moment of transaction. Wordless identity only works after memory has been earned. Removing the name is a governance decision about recognition equity, not a minimalist design trick.

Why is Mastercard a rebrand case?

Mastercard is filed as a rebrand case because the visible consequence sits in that decision pattern. A payment-network identity reached the point where the symbol could carry the name's job: acceptance, speed, trust, and global recognition at the moment of transaction.

What can brands learn from Mastercard?

Wordless identity only works after memory has been earned. Removing the name is a governance decision about recognition equity, not a minimalist design trick.

Is Mastercard still operating?

The Brand Archive marks Mastercard as Active / continuing. That means the brand, company, platform, product system, or parent organization is still operating, continuing, or being actively resolved.

What should Mastercard be compared with?

Compare Mastercard with Microsoft, Nickelodeon, Taco Bell to see the same decision pattern from nearby cases.