Brand System / Fintech / Buy now pay later / 2014-present

Afterpay Branding Strategy Case: Pay-in-4, Checkout, and Trust

Afterpay turned buy-now-pay-later into a branded checkout choice, then had to make the four-payment schedule, merchant value, spending controls, fees, and regulatory risk easy to inspect.

Short Answer

Afterpay Branding Strategy Case: Pay-in-4, Checkout, and Trust is a brand system case about Afterpay in 2014-present. Afterpay moved installment finance into the checkout moment and made the payment schedule the brand cue. A fintech brand cannot win on friction removal alone. If the product changes how people buy, the brand has to make cost, timing, limits, failed-payment consequences, merchant value, and customer control visible.

Reader Task

What this entry should help you finish

Use this entry to finish four jobs: answer what happened to Afterpay, see why it belongs in the brand system lane, inspect the decision consequence, and leave with the operator lesson. The point is not to remember the brand. The point is to know what decision, proof surface, or failure mode a team should check next. Then compare it with Nubank, Alibaba, Tencent before turning the case into a rule.

What Afterpay teaches

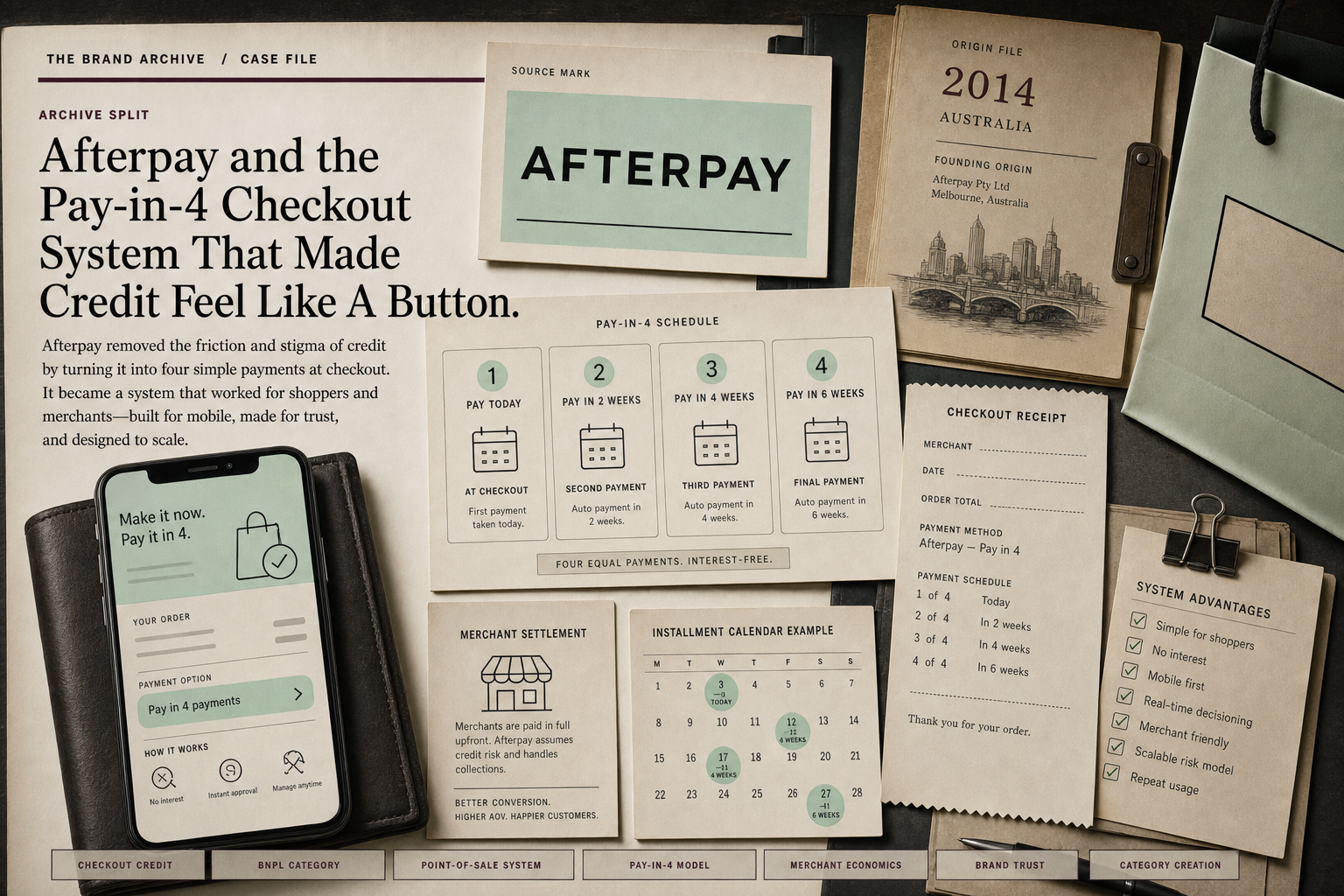

- Afterpay was founded in Australia in 2014.

- The brand's real move was placement: pay-in-4 appeared where the customer was already deciding, not in a separate credit application.

- The four-payment schedule is the trust device. It gives the customer a simple mental model before the purchase is approved.

- Merchant adoption gave the brand visibility, but consumer risk gave it a higher proof burden around fees, limits, hardship, refunds, and missed payments.

- Block's acquisition put Afterpay inside a larger commerce and payments stack, which changes the brand from checkout button to operating layer.

- The bad copycat copies BNPL conversion lift while hiding the customer-control problem.

Why This Brand Belongs In Grow Your Brand

Afterpay belongs in Grow Your Brand because the page studies a specific brand decision, not a company profile. The decision sits in brand system and gives operators a way to see how trust changes commercial value.

The useful archive question is what changed in recognition, trust, demand, pricing power, category position, or public memory after the market saw the move.

The Brand Asset At Stake

The asset at stake is access, transaction confidence, service recovery, and visible risk control. That asset matters because it affects how people find, understand, choose, trust, or repeat the brand when the company is not in the room to explain itself.

For Afterpay, the asset is not abstract equity. It has to show up in the buying surface, product surface, service route, source record, or repeated customer behavior.

What Changed

Afterpay moved installment finance into the checkout moment and made the payment schedule the brand cue.

The change forced the market to decide whether the old shortcut still worked, whether the new proof was strong enough, and whether the brand had made the category easier or harder to understand.

What The Market Learned

The market learned to judge Afterpay through the gap between the visible move and the proof behind it. calling the brand trusted while avoiding the proof of access, error handling, fees, service, and recovery is the weak reading this page is meant to prevent.

A useful brand decision makes buying, remembering, trusting, or repeating easier. A weak decision makes the audience do more work before it believes the claim.

Commercial Consequence

The commercial consequence sits in trust: access, transaction confidence, service recovery, and visible risk control. When that proof becomes easier to see, customers have more reason to choose, trust, repeat, or pay attention. When it becomes harder to see, the brand has to spend more money explaining what the market used to understand faster.

Afterpay matters because the decision changed more than presentation. It changed buyer confidence, memory, category position, or repeat behavior in fintech / buy now pay later. That is why the case belongs in a brand decision library instead of a general company profile.

What Another Brand Should Learn

Another brand should use this case before spending money on a similar move. Name the customer behavior, the proof surface, the protected cue, and the consequence that would make the decision worth the cost.

If the same proof does not exist in the business, copying Afterpay would copy the surface while missing the reason the decision mattered.

The Real Decision

Afterpay did not sell credit like a bank. It put a small payment choice inside retail checkout and made the repayment schedule simple enough to understand before the cart was finished.

That placement changed the brand job. Afterpay had to be both conversion tool for merchants and control signal for shoppers. If either side failed, the button would look like a trap rather than a convenience.

The Four-Payment Cue

The four-payment structure made the product legible. Customers could see the order split into a short schedule instead of a broad credit line or a vague promise to pay later.

That clarity is the useful brand asset. A customer deciding at checkout needs to know the payment dates, the approval path, the failed-payment consequences, the refund behavior, and the spending limit before the brand deserves trust.

The Merchant Side

Merchants adopted Afterpay because the button could change conversion, basket size, and checkout confidence. The brand became visible by sitting inside other retailers' purchase paths.

That visibility is powerful and risky. If the merchant uses BNPL to push weak demand, over-ordering, or unclear terms, the payment brand can inherit the customer's regret after the sale.

The Consumer Risk

BNPL brands have to explain more than ease. The customer needs to understand late fees, account holds, payment methods, returns, refunds, hardship paths, and what happens when several purchases stack at once.

This is where a checkout brand becomes a trust brand. The smoother the approval feels, the more explicit the repayment and recovery logic has to be.

Regulators Made The Proof Public

BNPL became large enough that regulators treated it as a consumer-finance category, not a harmless checkout decoration. Reports from consumer agencies put the same questions in public: repayment stacking, dispute handling, data use, fees, and whether users understand the obligation.

That public scrutiny changes the brand task. Afterpay has to make the product legible to shoppers, merchants, regulators, and parent-company stakeholders at the same time.

Block Changed The Context

Block completed its acquisition of Afterpay in 2022. That moved the brand into a wider commerce stack with seller tools, Cash App, payments, and merchant relationships.

The strategic test changed with ownership. Afterpay was no longer only a BNPL brand sitting beside merchants. It became part of a broader operating system where buyer finance, seller acceptance, and payment rails can reinforce one another or confuse the customer.

What People Get Wrong

The weak reading is that Afterpay won because it made credit easier. Ease is only half the story. The other half is whether the customer can see the trade before taking it.

The second weak reading is that BNPL is only a payments feature. In practice, it can change demand, cart behavior, return behavior, and customer cash-flow risk. That makes brand trust part of the product design.

The Bad Example

The bad copycat adds a pay-later button to checkout, advertises smaller payments, and hides the unpleasant details in policy pages.

That can lift conversion while weakening trust. Customers remember the late fee, refund confusion, account block, or stacked-payment surprise longer than they remember the smooth checkout.

What To Copy

Copy the visibility, not the temptation. Show payment dates, total cost, fee rules, refund behavior, account limits, and recovery paths in the decision moment.

A serious checkout-finance brand makes the trade obvious before approval. That protects the customer, the merchant, and the payment brand after the sale.

The Decision Limit

The Afterpay comparison is weak when the product does not change financial timing. If there is no customer risk, no merchant conversion pressure, and no repayment behavior, the BNPL lesson does not apply.

Use the case when a brand is moving a serious decision into a fast interface. The faster the interface, the clearer the proof has to be.

Compare Next

Related Cases

Do not read Afterpay alone. Compare it against nearby cases: Nubank, Alibaba, Tencent.

Sources

{kind=link}

People Also Ask

What happened to Afterpay?

Afterpay Branding Strategy Case: Pay-in-4, Checkout, and Trust is a brand system case about Afterpay in 2014-present. Afterpay moved installment finance into the checkout moment and made the payment schedule the brand cue. A fintech brand cannot win on friction removal alone. If the product changes how people buy, the brand has to make cost, timing, limits, failed-payment consequences, merchant value, and customer control visible.

Why is Afterpay a brand system case?

Afterpay is filed as a brand system case because the visible consequence sits in that decision pattern. Afterpay moved installment finance into the checkout moment and made the payment schedule the brand cue.

What can brands learn from Afterpay?

A fintech brand cannot win on friction removal alone. If the product changes how people buy, the brand has to make cost, timing, limits, failed-payment consequences, merchant value, and customer control visible.

Is Afterpay still operating?

Grow Your Brand marks Afterpay as Active / continuing. That means the brand, company, platform, product system, or parent organization is still operating, continuing, or being actively resolved.

What should Afterpay be compared with?

Compare Afterpay with Nubank, Alibaba, Tencent to see the same decision pattern from nearby cases.