Trust / Banking / payments / financial services / 1799-present

JPMorgan Chase and the Two-Layer Banking Trust System

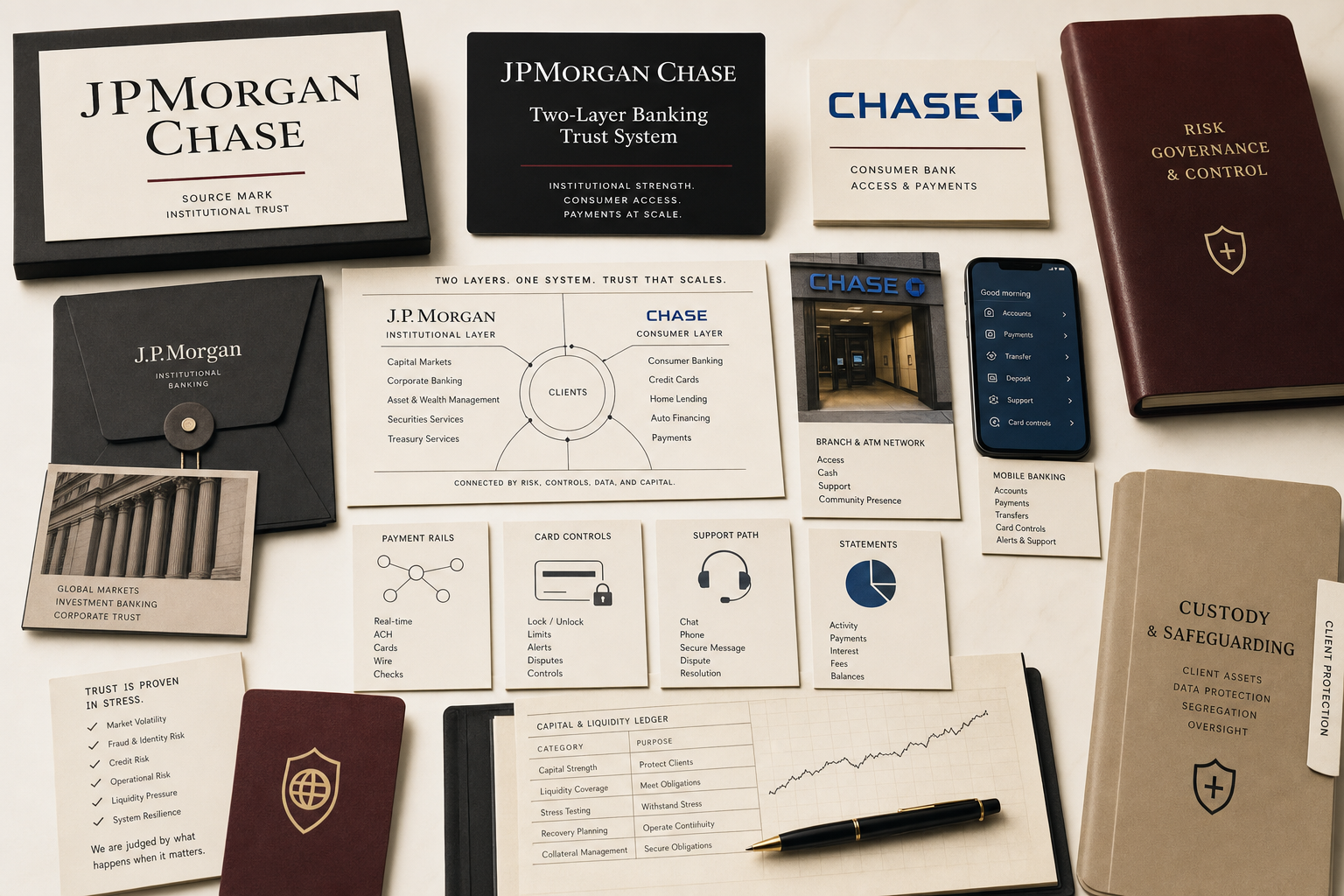

JPMorgan Chase carries institutional finance and consumer banking under one trust system: capital markets, cards, branches, payments, mobile access, fraud controls, custody, and risk governance.

Short Answer

JPMorgan Chase and the Two-Layer Banking Trust System is a trust case about JPMorgan Chase in 1799-present. JPMorgan Chase has to make two kinds of banking trust read as one system. Finance brands are judged when money, identity, access, fraud, credit, custody, and institutional risk are under pressure. The brand has to make both consumer convenience and institutional control visible.

Key Takeaways

- JPMorgan Chase carries the J.P. Morgan institutional memory and the Chase consumer banking and payments surface.

- The trust burden is two-layered: global finance and everyday money behavior sit under the same parent system.

- Branches, mobile banking, cards, payments, fraud controls, custody, and capital-market services all shape the brand.

- In banking, trust is proven when the customer can access money, recover from problems, and believe controls are real.

- The operator lesson is to separate the audience layers without letting them contradict the same trust promise.

The Decision Context

JPMorgan Chase is a trust case because the same company has to hold two public readings at once. J.P. Morgan carries institutional finance memory. Chase carries consumer banking, cards, payments, branches, and everyday access.

Both readings are about money, but they do not create trust the same way. An institution looks for risk control, custody, capital access, advisory depth, and continuity. A consumer looks for account access, card reliability, mobile control, fraud response, support, and a branch or human path when things go wrong.

Two Audiences, One Trust Burden

The brand architecture works only if the two layers do not fight each other. Institutional seriousness can make the consumer bank feel safer. Consumer reach can make the parent system feel embedded in daily life.

The risk runs the other way too. A failure in consumer access, fraud response, payments, compliance, or public conduct can travel upward. A banking brand cannot keep trust contained inside a single line of business.

Payments And Access Are Proof

For most customers, banking trust is not an abstract capital-strength claim. It is whether the card works, the transfer arrives, the login opens, the statement makes sense, the fraud alert helps, and support knows what to do.

Those ordinary surfaces are brand architecture. They make a large financial institution either feel dependable or distant.

The Archive Reading

JPMorgan Chase belongs in the archive because it shows how a financial brand can carry institutional authority and consumer habit at the same time.

For operators, the lesson is to design the trust layers. The expert audience and the everyday user may need different signals, but they still test the same promise under pressure.

Comparable Cases

Sources

People Also Ask

What happened to JPMorgan Chase?

JPMorgan Chase and the Two-Layer Banking Trust System is a trust case about JPMorgan Chase in 1799-present. JPMorgan Chase has to make two kinds of banking trust read as one system. Finance brands are judged when money, identity, access, fraud, credit, custody, and institutional risk are under pressure. The brand has to make both consumer convenience and institutional control visible.

Why is JPMorgan Chase a trust case?

JPMorgan Chase is filed as a trust case because the visible consequence sits in that decision pattern. JPMorgan Chase has to make two kinds of banking trust read as one system.

What can brands learn from JPMorgan Chase?

Finance brands are judged when money, identity, access, fraud, credit, custody, and institutional risk are under pressure. The brand has to make both consumer convenience and institutional control visible.

Is JPMorgan Chase still operating?

The Brand Archive marks JPMorgan Chase as Active / continuing. That means the brand, company, platform, product system, or parent organization is still operating, continuing, or being actively resolved.

What should JPMorgan Chase be compared with?

Compare JPMorgan Chase with American Express, Visa, Mastercard to see the same decision pattern from nearby cases.