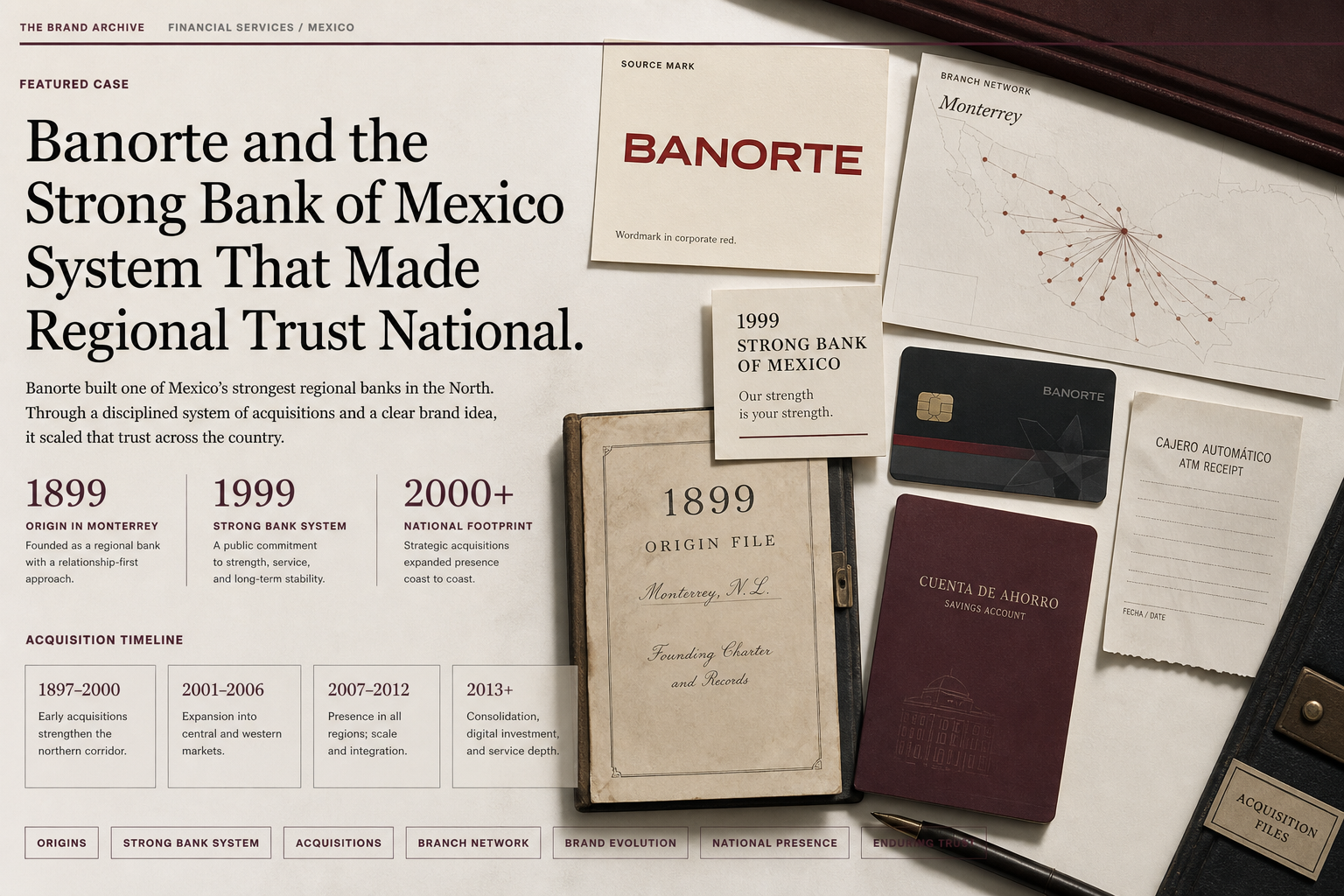

Brand System / Banking / Financial trust / 1899-present

Banorte Branding Case: Mexican Banking Trust and Access

Banorte is the banking-trust case for turning regional origin, Mexican ownership memory, branch and ATM access, digital banking, financial group scale, and strong-bank language into national confidence.

Short Answer

Banorte Branding Case: Mexican Banking Trust and Access is a brand system case about Banorte in 1899-present. Banorte works when strength is visible to customers through reach, account access, digital tools, local understanding, financial group breadth, and service reliability. Bank strength has to become usable proof. Customers need to see where money moves, where help exists, how digital access works, and why the institution deserves trust.

Reader Task

What this entry should help you finish

Use this entry to finish four jobs: answer what happened to Banorte, see why it belongs in the brand system lane, inspect the decision consequence, and leave with the operator lesson. The point is not to remember the brand. The point is to know what decision, proof surface, or failure mode a team should check next. Then compare it with Nubank, Itaú, Sber before turning the case into a rule.

What Banorte teaches

- Banorte is a trust-and-scale case because the brand asks customers to read strength as safety and reach.

- Regional origin can help when it anchors local confidence instead of limiting national ambition.

- Branches, ATMs, cards, digital banking, and group services turn strength into daily use.

- The weak copycat says strong bank while leaving access, service, and proof vague.

- The repair test is whether customers can connect the strength claim to money movement and support.

Why This Brand Belongs In Grow Your Brand

Banorte belongs in Grow Your Brand because the page studies a specific brand decision, not a company profile. The decision sits in brand system and gives operators a way to see how trust changes commercial value.

The useful archive question is what changed in recognition, trust, demand, pricing power, category position, or public memory after the market saw the move.

The Brand Asset At Stake

The asset at stake is access, transaction confidence, service recovery, and visible risk control. That asset matters because it affects how people find, understand, choose, trust, or repeat the brand when the company is not in the room to explain itself.

For Banorte, the asset is not abstract equity. It has to show up in the buying surface, product surface, service route, source record, or repeated customer behavior.

What Changed

Banorte works when strength is visible to customers through reach, account access, digital tools, local understanding, financial group breadth, and service reliability.

The change forced the market to decide whether the old shortcut still worked, whether the new proof was strong enough, and whether the brand had made the category easier or harder to understand.

What The Market Learned

The market learned to judge Banorte through the gap between the visible move and the proof behind it. calling the brand trusted while avoiding the proof of access, error handling, fees, service, and recovery is the weak reading this page is meant to prevent.

A useful brand decision makes buying, remembering, trusting, or repeating easier. A weak decision makes the audience do more work before it believes the claim.

Commercial Consequence

The commercial consequence sits in trust: access, transaction confidence, service recovery, and visible risk control. When that proof becomes easier to see, customers have more reason to choose, trust, repeat, or pay attention. When it becomes harder to see, the brand has to spend more money explaining what the market used to understand faster.

Banorte matters because the decision changed more than presentation. It changed buyer confidence, memory, category position, or repeat behavior in banking / financial trust. That is why the case belongs in a brand decision library instead of a general company profile.

What Another Brand Should Learn

Another brand should use this case before spending money on a similar move. Name the customer behavior, the proof surface, the protected cue, and the consequence that would make the decision worth the cost.

If the same proof does not exist in the business, copying Banorte would copy the surface while missing the reason the decision mattered.

The Decision Context

Banorte has to make strength practical. A bank can speak about national scale and Mexican trust, but customers judge the brand when money has to move, be protected, borrowed, saved, or recovered.

That makes Banorte a useful banking case. The brand has to connect history, branch reach, digital access, cards, financial group services, and service reliability.

Strength Needs A Customer Translation

Strong-bank language is useful only when the customer can see what it protects. Does it mean available branches, stable digital access, credible credit, clear statements, fraud support, or easier service?

The translation matters because banking trust is not abstract. It is judged during payments, account questions, loans, lost cards, retirement decisions, and business needs.

Regional Origin Can Support National Trust

Banorte's northern and Mexican ownership memory gives the brand a local confidence layer. That can strengthen the institution when national banking choices read interchangeable.

The origin cue has to point forward. Customers still need modern access, digital convenience, and reliable service.

Channels Carry The Brand

Branches, ATMs, cards, apps, call centers, and advisor routes all carry the trust promise. A bank brand is experienced as a channel system.

If one channel breaks, the strength claim is tested. The customer wants a clear way to solve the problem.

Where The Strategy Breaks

The strategy breaks when strength becomes slogan language. A customer cannot deposit money into a slogan or recover a failed transaction through a patriotic line.

It also breaks when national scale creates distance. Big-bank trust still needs reachable service.

The Bad Copycat

A bad copycat would copy red banking cues, national language, and strength claims while leaving the actual service path ordinary.

That creates confidence theatre. In banking, the proof appears when the customer needs access, answer, protection, or correction.

The Signal Reading

Banorte is filed here because it records how banking trust must convert scale and origin into usable customer confidence.

The decision test is whether the brand can answer where money is, how it moves, who helps, and what happens when risk appears.

The Evidence Standard

The evidence standard is whether strength becomes useful to customers. A bank can claim scale, local ownership, and national trust, but the proof is account access, payment confidence, lending clarity, and service recovery.

Branch and ATM proof matter because banking trust is still physical for many customers. The customer needs to know where help and money access are available.

Digital proof matters because the app, login, transfer, card controls, alerts, and support paths now carry much of the brand. A strong bank with unclear digital service creates doubt.

Group proof matters because financial groups can offer banking, brokerage, insurance, retirement, and business services. The architecture should guide the customer rather than bury them in options.

The weak page would repeat strong-bank language. The stronger page asks what the strength protects in a money-risk moment.

A useful check would inspect branch access, digital banking, account pages, investor reporting, service language, and product architecture. These tell customers what strength means.

The decision lesson is to translate institutional scale into customer confidence. Pride and national presence matter only when they make financial decisions safer to navigate.

The page earns its place when it teaches banking brands to prove strength through access, clarity, and correction.

Reader Inspection

Read Banorte through the Mexican banking trust system, then ask what problem the customer or buyer had before the system existed.

The primary risk is strength language without service proof, channel confusion, product sprawl, digital doubt, and weak correction paths. If the page does not name that risk, it becomes brand admiration rather than brand analysis.

Inspect the public surfaces: branches, ATMs, digital banking, account pages, investor reporting, service language, cards, and financial-group architecture. Those are the places where the promise is either proved or exposed.

The strongest evidence is behavioral. The page should explain what a buyer can do with less doubt because Banorte organized the decision differently.

The weak version copies the visible cue and skips the operating proof. That mistake creates a nicer surface while leaving the customer's original uncertainty in place.

A useful case should state what to check before copying the move. The check has to include the product path, the service path, the failure path, and the source trail.

The proof threshold is simple: the customer can connect institutional strength to a specific money-risk moment. If that cannot be seen, the brand idea is still too vague to teach.

Use this case as a decision lens, not as a style reference. The point is to understand which operating behavior made the brand easier to choose, trust, or repeat.

Compare Next

Related Cases

Do not read Banorte alone. Compare it against nearby cases: Nubank, Itaú, Sber.

Sources

{kind=link}

People Also Ask

What happened to Banorte?

Banorte Branding Case: Mexican Banking Trust and Access is a brand system case about Banorte in 1899-present. Banorte works when strength is visible to customers through reach, account access, digital tools, local understanding, financial group breadth, and service reliability. Bank strength has to become usable proof. Customers need to see where money moves, where help exists, how digital access works, and why the institution deserves trust.

Why is Banorte a brand system case?

Banorte is filed as a brand system case because the visible consequence sits in that decision pattern. Banorte works when strength is visible to customers through reach, account access, digital tools, local understanding, financial group breadth, and service reliability.

What can brands learn from Banorte?

Bank strength has to become usable proof. Customers need to see where money moves, where help exists, how digital access works, and why the institution deserves trust.

Is Banorte still operating?

Grow Your Brand marks Banorte as Active / continuing. That means the brand, company, platform, product system, or parent organization is still operating, continuing, or being actively resolved.

What should Banorte be compared with?

Compare Banorte with Nubank, Itaú, Sber to see the same decision pattern from nearby cases.